Our Core Features

New Models for Economics

Granularity, Interconnectedness & Complexity

Agent Based Simulations and Applications of AI

Computational Macro Economics, Computational Micro Economics

Database Driven Models

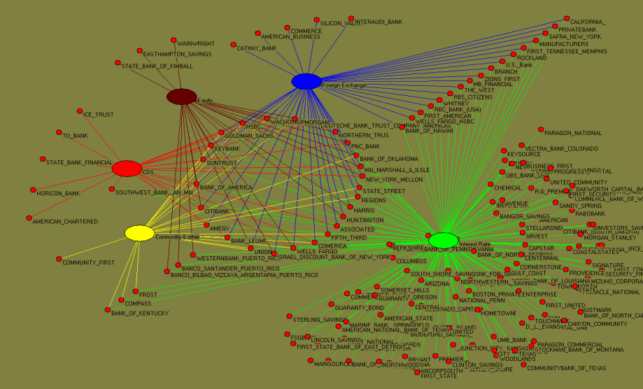

Big Data & Bilateral Who-Whom Data

Real Time systems & Electronic Markets

London Electronic Trading Systems, Artificial Stock Markets

Our Projects

More Features

Download the Simulators

You can download the simulators

Run the Simulators

You can virtually run our simulators

Some of our Connections

What they say about us

2017 Eubank Prize by the Rice University , Houston , USA

2017 Eubank Prize

Sheri published paper on How Digital Agents Innovate