Systemic Risk from Financial Derivatives

In 2011, in an IMF project Sheri led on Systemic Risk from Global Financial Derivatives Markets using network analysis, an iconic graph based on our CCFEA financial network software showed, for the first time, the fallacy of composition at the heart of modern financial risk management. Despite what seems rational at the level of an individual financial institution to use derivatives to move risk from its balance sheet to a guarantor, the system as a whole is unstable as risk is concentrated at the core of the global network in the hands of 16 broker dealers (such as Goldman Sachs, JP Morgan, HSBC, Bank of America etc). This threat continues.

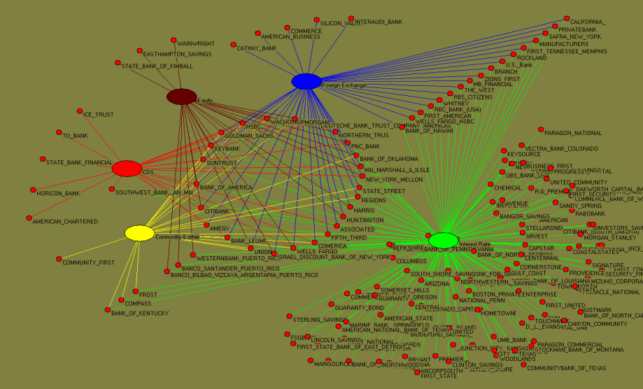

The first paper published on this subject is the 2012 IMF Working paper from Sheri Markose, “Systemic Risk from Global Financial Derivatives : A Network Analysis of Contagion and Its Mitigation with Super-Spreader Tax”. The above network of financial derivatives is taken from the Markose (2012) IMF Working Paper, detailing the affiliation graph of global SIFIs and United States (U.S.) FDIC FIs and participants in the five financial derivatives markets. The key denotes the colour associated with each derivative market.

This work began with looking at US centric FDIC data on financial derivatives trading only activities for 2009 Q4. There is a data gap on non-US participants in derivatives markets to obtain data of the same quality as that in the FDIC Call Reports. As there is no single source for large non- US banks and other financial participants in the derivatives markets, the next step of the project will include the data collected individually from the Annual Financial Reports of non US participants. The US centric network of financial obligations is built on the basis of a preferential attachment model driven by the empirical market share of gross notional of derivatives. The bilateral flows are determined by the OCC GPFV and GNFV data and constrained to satisfy the fim level empirical data on bilaterally netted amounts leading to derivatives liabilities and assets.

In light of above data gaps, who-whom bilateral data on balance sheet linkages between financial players should be mandated and digitally mapped to avoid model error.

See here for presentation slides.

See here for 2017 lectures at RICE university: “On Interconnectedness and Systemic Risk in Derivatives: Updates on G20 OTC Reforms and skin-in-the game for CCPs.”

For more papers, see the Research and Applications section.